U.S. Manufacturing Inventory Census Report

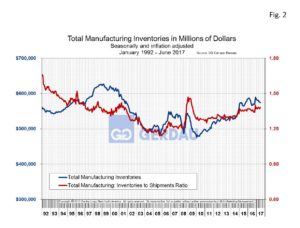

Total seasonally adjusted (SA), non-inflation adjusted manufacturing inventories totaled $649,086 million (M) at the end of June, up 0.16% month on month, (m/m) and up 4.78% year on year, (y/y). The total manufacturing inventories to shipment ratio, (I/S) was up 0.01 to 1.38 m/m and up 0.03 percentage points y/y.

The US Census Bureau issues a report on inventory levels of manufactured goods. The time series data is presented in both seasonally adjusted (SA), non-inflation adjusted dollars and inflation adjusted dollars. The inflation adjustment is made by using the Census Bureau’s producer price index (PPI), series for each of its nine categories.

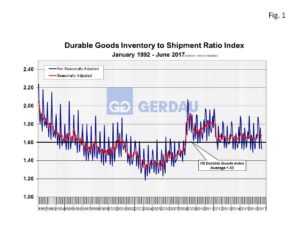

Figure 1 presents the I/S ratio for durable goods inventory in both SA and NSA format for, 1992 to present. The SA, I/S was 1.68 in June. It has been within 0.02 points of this value for the last seven months. The ratio averaged 1.65 for the first six months of 2016. A smaller ratio results in higher inventory turns and a faster cash to cash cycle.

Figure 1 presents the I/S ratio for durable goods inventory in both SA and NSA format for, 1992 to present. The SA, I/S was 1.68 in June. It has been within 0.02 points of this value for the last seven months. The ratio averaged 1.65 for the first six months of 2016. A smaller ratio results in higher inventory turns and a faster cash to cash cycle.

The SA, I/S ratio came steadily down throughout the 1990s and early 2000s. Information technology and higher productivity gets most of the credit for this improvement. When the recession hit, the I/S ratio jumped as consumers cut their spending, inventories climbed and layoffs ensued. In March 2012 the SA, I/S corrected falling from 1.80 in February to 1.63 by year end. Since then it has been in a narrow range between 1.61 and 1.70.

Figure 2 examines manufacturing inventories from 1992 to present, (blue line, left-hand Y axis), and it’s I/S ratio (red line, right-hand Y axis). So far in 2017, inventory levels are climbing modestly, while at the same time the I/S ratio is relatively flat. It is a sign of confidence for the manufacturing sector when the blue line is higher than the red line as it the present-day case.

examines manufacturing inventories from 1992 to present, (blue line, left-hand Y axis), and it’s I/S ratio (red line, right-hand Y axis). So far in 2017, inventory levels are climbing modestly, while at the same time the I/S ratio is relatively flat. It is a sign of confidence for the manufacturing sector when the blue line is higher than the red line as it the present-day case.

Automobile manufacturing SA adjusted non-inflation adjusted inventories were $4,469M, 3.4% higher m/m, but down 9.4% y/y. June light truck manufacturing SA adjusted inventories were $3,625M, off 1.1% m/m and down 7.3% y/y. Meanwhile, heavy truck manufacturing SA adjusted inventories were $2,088M, 2.7% higher m/m, and up 6.2% y/y.

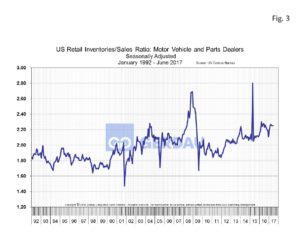

Figure 3 shows SA retail I/S ratio of vehicles and parts from 1992 to present. The I/S ratio was 2.25 in June, flat (within + or - 0.01), m/m and y/y, but generally trending higher. Data from Ward’s automotive supports this, reporting that days-supply in July was 69, up 8 days y/y. Sales through July on a SA annualized rate, (SAAR) were 16.41M units down 0.5% from June 2016s SAAR of 16.5M units.

shows SA retail I/S ratio of vehicles and parts from 1992 to present. The I/S ratio was 2.25 in June, flat (within + or - 0.01), m/m and y/y, but generally trending higher. Data from Ward’s automotive supports this, reporting that days-supply in July was 69, up 8 days y/y. Sales through July on a SA annualized rate, (SAAR) were 16.41M units down 0.5% from June 2016s SAAR of 16.5M units.

Iron and steel mill inventories (includes ferroalloys & steel products manufacturing), totaled $17,104M in June, up 0.7% m/m but were down 0.3% y/y. Iron and steel mill inventories represented 3.0% of total manufacturing inventories in June.

At Gerdau, we periodically review the Census Bureau’s inventory report to get a gauge on how manufacturing is currently performing and to get a read on likely future outcomes.