U.S. Inventory Census Report

Total seasonally adjusted (SA), inflation adjusted manufacturing inventories totaled $576,243 million (M) at the end of May, flat month on month (m/m), but up 0.6% year on year, (y/y).The total manufacturing inventories to shipment ratio (I/S), was 1.38 flat m/m and up 0.02 points y/y.

The US Census Bureau issues a report on inventory levels of manufactured goods. The time series data is presented in both seasonally adjusted (SA), non-inflation adjusted dollars and inflation adjusted dollars. The inflation adjustment is made by using the Census Bureau’s producer price index (PPI), series for each of its nine categories.

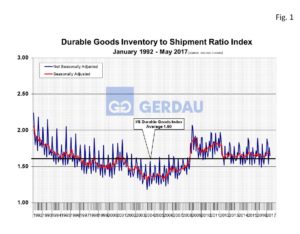

Figure 1 presents the I/S ratio for durable goods inventory in both SA and NSA format for, 1992 to present. The SA I/S was 1.68 in May. It has been within 0.1 points of this value for the last six months. The ratio averaged 1.65 for the first five months of 2016. A smaller ratio results in higher inventory turns and a faster cash to cash cycle.

Figure 1 presents the I/S ratio for durable goods inventory in both SA and NSA format for, 1992 to present. The SA I/S was 1.68 in May. It has been within 0.1 points of this value for the last six months. The ratio averaged 1.65 for the first five months of 2016. A smaller ratio results in higher inventory turns and a faster cash to cash cycle.

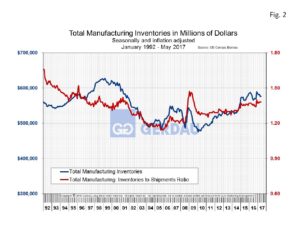

Figure 2 examines manufacturing inventories from 1992 to present, (blue line, left-hand Y axis), and it’s I/S ratio (red line, right-hand Y axis). So far in 2017, inventory levels are climbing modestly, while at the same time the I/S ratio is falling. When the blue line is higher than the red line inventories are building. This can be a sign of confidence that future sales will absorb the inventory build. It can also mean that sales are slowing relative to production. In this case, if sales do not pick-up production will have to be curtailed.

examines manufacturing inventories from 1992 to present, (blue line, left-hand Y axis), and it’s I/S ratio (red line, right-hand Y axis). So far in 2017, inventory levels are climbing modestly, while at the same time the I/S ratio is falling. When the blue line is higher than the red line inventories are building. This can be a sign of confidence that future sales will absorb the inventory build. It can also mean that sales are slowing relative to production. In this case, if sales do not pick-up production will have to be curtailed.

Motor vehicles and parts SA and inflation adjusted inventories were $31,449M, 5.5% of total manufacturing inventories. Figure 3  shows SA and inflation adjusted retail I/S ratio of vehicles and parts from 1992 to present. The I/S ratio was 2.26 in May, flat (within + or - 0.01), m/m and y/y, but generally trending higher. The I/S ratio averaged 2.16 in 2015 and 2.22 in 2016. Year to date in 2017, the I/S ratio averaged 2.24. Data from Ward’s automotive supports this, reporting that days-supply in June was 74, up 8 days y/y. Sales through June were at an SA annualized rate of 16.41M. Unit sales in June were 466,873, down 5.4% from 475,037 in June 2016.

shows SA and inflation adjusted retail I/S ratio of vehicles and parts from 1992 to present. The I/S ratio was 2.26 in May, flat (within + or - 0.01), m/m and y/y, but generally trending higher. The I/S ratio averaged 2.16 in 2015 and 2.22 in 2016. Year to date in 2017, the I/S ratio averaged 2.24. Data from Ward’s automotive supports this, reporting that days-supply in June was 74, up 8 days y/y. Sales through June were at an SA annualized rate of 16.41M. Unit sales in June were 466,873, down 5.4% from 475,037 in June 2016.

Iron and steel mill inventories (includes ferroalloys & steel products manufacturing), totaled $17,052M in May, up 1.1% m/m, flat y/y. Iron and steel mill inventories were 3% of total manufacturing inventories.

At Gerdau, we periodically review the Census Bureau’s inventory report to get a gauge on how manufacturing is currently performing and to get a read on likely future outcomes.