U.S. Housing Starts and Permits

Total housing starts were reported at a seasonally adjusted (SA), annual rate of 1,155,000 for the month of July, down 4.8% month on month, (m/m). On a three month moving average (3MMA), basis SA total starts came-in at 1,166,000, a negative 1.2% year on year (y/y), growth rate. Single family housing starts jumped by 10.7%, 3MMA y/y, while multi-family tumbled by 22.5%, 3MMA y/y.

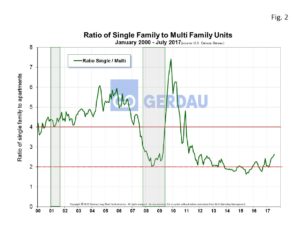

Figure 1 shows SA housing starts history from 2011 to present. The split of single family (SF), to multi-family (MF) starts was 71.8% SF to 18.2% MF. The volume of SF vs. MF starts has shifted strongly in favor of SF over past twelve months. In July 2015 the split was 65.2% SF to 14.8% MF. Figure 2

Figure 1 shows SA housing starts history from 2011 to present. The split of single family (SF), to multi-family (MF) starts was 71.8% SF to 18.2% MF. The volume of SF vs. MF starts has shifted strongly in favor of SF over past twelve months. In July 2015 the split was 65.2% SF to 14.8% MF. Figure 2 illustrates the ratio of SF to MF from 2000 to present. Pre-recession the ratio of SF:MF was in the 5:1 to 6:1 range. This ratio plummeted after the recession as demand shifted intensely to apartments. The ratio fell below 2:1 throughout most of 2014 and 2015 and is now trending higher, reaching 2.63:1 in July. The ratio has been higher in each of the past five months. This shift means that consumers are gaining confidence in the strength of the housing market.

illustrates the ratio of SF to MF from 2000 to present. Pre-recession the ratio of SF:MF was in the 5:1 to 6:1 range. This ratio plummeted after the recession as demand shifted intensely to apartments. The ratio fell below 2:1 throughout most of 2014 and 2015 and is now trending higher, reaching 2.63:1 in July. The ratio has been higher in each of the past five months. This shift means that consumers are gaining confidence in the strength of the housing market.

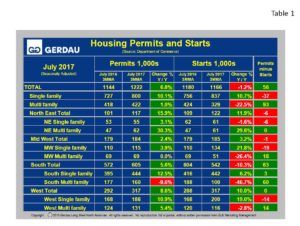

The South has by far the highest number of starts with 542,000, 3MMA annualized starts, 46.4% of the last 3 months total. However, trend has been downward with each of the last four months lower than the previous month. On a y/y comparison the growth rate of housing starts has declined by 10.3%. The West was the next largest with 317,000 starts, a 27.3% share of starts. The West’s growth rate of starts was up 10.0% y/y. The Midwest started 185,000 housing units, 15.9% of the total, its housing starts growth was up 3.2% y/y. The Northeast had 122,000 starts representing with 10.4% of the total 3MMA annualized starts. The Northeast’s’ 11.9% y/y rate of starts growth was the strongest of the four regions in July.

Table 1 breaks down starts and permit detail for SF and MF by region. All data references are three month moving averages y/y, (3MMA y/y), which helps smooth out spikes in single month data and therefore gives a more realistic viewpoint on the pulse of home building activity. Nationally, SA, SF starts were up 10.7% y/y. SF starts in the Northeast surged 1.6%. SF starts were up 21.8% in the Midwest, up 6.2% in the South and up 19% in the West. Nationally, SA, MF starts plunged 22.5%. MF starts in the Northeast surged higher by 29.6%, while SF starts tumbled 26.4% in the Midwest, plunged by 46.7% in the South and fell by 2.8% in the West.

Table 1 breaks down starts and permit detail for SF and MF by region. All data references are three month moving averages y/y, (3MMA y/y), which helps smooth out spikes in single month data and therefore gives a more realistic viewpoint on the pulse of home building activity. Nationally, SA, SF starts were up 10.7% y/y. SF starts in the Northeast surged 1.6%. SF starts were up 21.8% in the Midwest, up 6.2% in the South and up 19% in the West. Nationally, SA, MF starts plunged 22.5%. MF starts in the Northeast surged higher by 29.6%, while SF starts tumbled 26.4% in the Midwest, plunged by 46.7% in the South and fell by 2.8% in the West.

Nationally, total SA annualized permits increased 6.8%, 3MMA y/y to 1,222,000 units with SF permits up 10.1% and MF permits up 1.0%. All regions reported stronger growth in total building permits y/y.

The Northeast reported a 15.9% y/y rise in permits, a combination of a 3.9% increase for SF and a 15.9% y/y gain for MF. The Midwest total permits were up 2.4% y/y (SF +3.9%, MF flat), while the South posted overall permit growth of 5.6%, (SF +12.5%, MF -9.6%). The West saw its residential permits increase by 8.6%, (SF +10.9% y/y, MF 5.4%).

Permits gage future housing builds. The column on the far right in Table1 illustrates permits minus starts. For the nation as a whole permits minus starts = +56,000. This indicates that housing construction will rise in the coming months.

At Gerdau, we routinely monitor the US housing market because historically new home construction has preceded non-residential construction and therefore is an excellent barometer to foresee the likely future demand for construction steel products.