Consumer Credit

Total consumer credit increased by $18.4 billion, (B) in December, below the consensus estimate of $20B. Non-revolving credit advanced by $13.3B while revolving credit moved-up by $5.3B. November’s consumer credit was revised upwards by $2B to $30B essentially offsetting the miss in December.

On a percentage year on year basis, consumer credit increased at an annual rate of 5.4%. Revolving credit increased at an annual rate of 6.0% percent, while Nonrevolving credit increased at an annual rate of 5.1% percent.

Consumer credit represents loans for households, for financing consumer purchases of goods and services, and for refinancing existing consumer debt. Secured and unsecured loans are included, except those secured with real estate (such as mortgages and home equity loans and lines). The two categories of consumer credit are revolving and Nonrevolving debt. Revolving debt covers credit card use for purchases or cash advances, store charge accounts. Nonrevolving includes auto loans, personal and student loans and other miscellaneous items such as recreation vehicle loans.

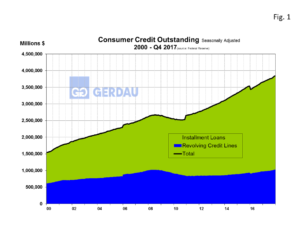

Figure 1 shows consumer credit outstanding from 2000 to present. The blue area represents revolving credit, while installment loans, is illustrated by the green fill. Consumers have been more careful with revolving credit since the great recession, the current level is just now reaching the peak achieved in 2008.

Figure 1 shows consumer credit outstanding from 2000 to present. The blue area represents revolving credit, while installment loans, is illustrated by the green fill. Consumers have been more careful with revolving credit since the great recession, the current level is just now reaching the peak achieved in 2008.

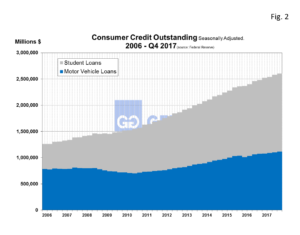

Figure 2  presents motor vehicle and student loans on the same chart. Student loans have expanding at more rapid rate than vehicle loans since the mid-2000s. In 2006 the ratio of student loans to auto loans was 0.40 to 0.60. By 2010 this ratio had shifted to 0.55 to 0.45. Last year in the student loan ratio increased to 0.57, so the gap continues to widen. In Q4, motor vehicle loans grew by 3.8% year on year, while student loans increased by 5.9% year on year.

presents motor vehicle and student loans on the same chart. Student loans have expanding at more rapid rate than vehicle loans since the mid-2000s. In 2006 the ratio of student loans to auto loans was 0.40 to 0.60. By 2010 this ratio had shifted to 0.55 to 0.45. Last year in the student loan ratio increased to 0.57, so the gap continues to widen. In Q4, motor vehicle loans grew by 3.8% year on year, while student loans increased by 5.9% year on year.

Consumers continue to spend freely as their confidence in the economy is high. Consumers slowed their spending habits a bit in December after November posted the strongest gain on record. Consumers have the ability to take on additional debt as the current level of debt burden is near its lowest level in 35 years. In addition delinquency and default rates are also at historically low rates.

Risks on the horizon include the uncertainty surrounding the healthcare marketplace and geopolitical tensions. Higher interest rates could also present challenges since debt servicing will rise on revolving credit, while higher borrowing costs will inhibit growth in both the home mortgage and auto markets.

At Gerdau, we monitor consumer spending because history has shown that increased consumer spending (approximately 69% of GDP), translates into increased steel consumption (and vice versa).