Construction Put-in-Place, (CPIP)

Total U.S. construction spending came in above the consensus estimate in December. This was the fifth month in a row of gains in construction expenditures. Census Bureau non-seasonally adjusted (NSA), constant dollar CPIP data showed that December’s twelve month total, (12MT) construction expenditures grew by 3.6% year on year (y/y), to $1226.9 billion (B). On a 12MT basis, private expenditures advanced 5.8% y/y, while, State & Local contracted by 2.4% y/y. Non-residential 12MT CPIP increased by 1.8% y/y to $569.0B.

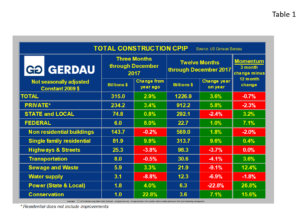

Total Construction:  Table 1 presents CPIP data for total construction for both 3 moving total and 12 month moving total y/y metrics. Momentum, defined as 3MT minus 12MT is also shown. Momentum provides market direction with green indicating stronger activity and red indicating slowing activity. Private construction accounted for 74.3% of the total three months expenditures ending in December. State & local spending accounted for 23.8%, the remaining 1.9% was for federally financed projects. The private sector posted 3.4% and 5.8% growth for 3MT and 12MT y/y comparisons resulting in negative 2.3% momentum for the month of December.

Table 1 presents CPIP data for total construction for both 3 moving total and 12 month moving total y/y metrics. Momentum, defined as 3MT minus 12MT is also shown. Momentum provides market direction with green indicating stronger activity and red indicating slowing activity. Private construction accounted for 74.3% of the total three months expenditures ending in December. State & local spending accounted for 23.8%, the remaining 1.9% was for federally financed projects. The private sector posted 3.4% and 5.8% growth for 3MT and 12MT y/y comparisons resulting in negative 2.3% momentum for the month of December.

Single family residential construction recorded 9.9% growth on a 3MT basis, stronger than the 9.6%, 12MT y/y score, resulting in positive momentum. A momentum score of +2.8% indicates continue growth going forward. Residential construction is the largest segment, accounting for 46.4% of total construction outlays. Private residential spending has been a strong performer in 2017, and rebuilding activity from the fall hurricanes is expected enhance outlays throughout 2018. Nationally there is a significant undersupply of existing homes causing prices to rise. A strong job market, low interest rates and pent-up demand is driving demand. This trend is expected to continue in 2018.

On 12MT basis, State and Local total construction was in the red, off 2.4%. However on a 3MT month y/y basis, State and Local total construction recorded a 0.8% increase in spending. This was the second month in a row of positive growth on a 3MT y/y basis, after a string of 17 months of negative numbers. In a further encouraging sign, momentum was +3.2%.

The infrastructure project groups recorded negative growth on a 12MT y/y comparison for all groups except Conservation which was higher by 7.1%. On an optimistic note, every category recorded positive momentum in December except Water Supply, (-1.8%) indicating that spending is accelerating. Sewage and waste and Power (State & Local) and Conservation all posted positive 3MT y/y expenditures measuring; +3.3%, +4.0% and +22.8% respectfully.

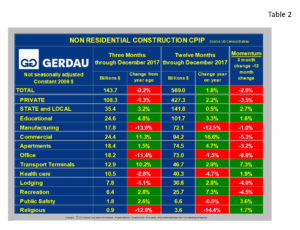

Non-residential Construction: Table 2  shows the breakdown of non-residential construction (NRC). The overall growth rate was negative 0.2% on a 3MT y/y basis and +1.8% on a 12MT y/y comparison resulting in negative 2.0% momentum.

shows the breakdown of non-residential construction (NRC). The overall growth rate was negative 0.2% on a 3MT y/y basis and +1.8% on a 12MT y/y comparison resulting in negative 2.0% momentum.

The growth rate of private NRC was negative 1.3% for the 3MT ending December, less than the rolling 12MT value of +2.2%, leading to negative momentum of -3.5%. This is the fourth month in a row that the 3MT y/y growth rate has been negative after 74 months in the positive column.

State and local expenditures were positive for both 3MT and 12MT metrics. The 3MT y/y increase was +3.2%, much stronger than the 0.5%, 12MT y/y growth giving rise to positive momentum of +2.7%. December’s positive percentage posting marks four consecutive months of growth on 3MT y/y basis and three months in a row of positive percentage growth on a 12MT y/y comparison.

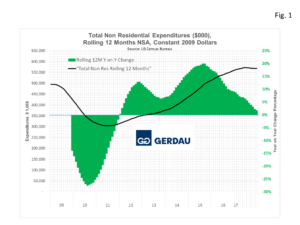

Figure 1 charts the NSA rolling 12MT expenditure history for non-residential construction from 2009 to present. Expenditures (black line) are read on the left Y axis in constant 2009 dollars. The year on year change, (green bars) are read off the right Y axis. Total non-residential expenditures was recently at its highest point since our data began. It has now started to plateau. While expenditures remain at elevated levels, the y/y percentage change is on a continuous downward slope.

Figure 1 charts the NSA rolling 12MT expenditure history for non-residential construction from 2009 to present. Expenditures (black line) are read on the left Y axis in constant 2009 dollars. The year on year change, (green bars) are read off the right Y axis. Total non-residential expenditures was recently at its highest point since our data began. It has now started to plateau. While expenditures remain at elevated levels, the y/y percentage change is on a continuous downward slope.

Looking at the project categories within non-residential buildings, some are exhibiting strong growth while others are declining. Educational, Commercial, Apartments (>4 stories), Recreation and Transportation terminal construction all recorded positive growth on both 3MT and 12MT y/y metrics.

Educational structures posted percentage increases of 4.8% y and 3.3% for 3MT y/y and 12MT y/y respectfully. Commercial construction was up 11.3%, 3MT y/y and +16.6%, 12MT y/y. Apartment construction is still increasing albeit at a slower rate on the 3MT y/y metric, (+1.5%) vs. the 12MT y/y comparison at 4.7%. Values of +2.8% and +7.3% for 3MT y/y and 12MT y/y growth were posted for Recreation projects. Transportation terminal recorded strong 3MT y/y growth of +10.2%, far stronger than the +2.9% growth measured on a 12MT basis leading a strong momentum score of +7.3%.

Sectors that are recording contracting expenditures on both rolling 3MT and 12MT y/y comparisons, include: manufacturing buildings, office buildings, healthcare, and religious structures.

Manufacturing buildings recorded the weakest performance, down 13.6% and 12.5% for 3MT y/y and 12MT y/y respectfully. Three month y/y total expenditures have been in the negative column for 20 months in a row. Prior to that there was a 57 consecutive month period of strong growth in this sector. After a solid performance last year, office construction is starting to wane, off 11.4%, 3MT y/y and -1.5%, 12MT y/y. Momentum was negative 9.9% as a result of the large change between the two periods. Healthcare recorded -2.8%, 3MT y/y and -4.7%, 12MT y/y. Religious structures, -12.8%, 3MT y/y and -14.4%, 12MT y/y.

Overall the construction market continues to perform well exhibiting continuing y/y growth from the private sector. Public sector spending moved-up strongly in December is a hopeful sign that we will see a rebound in spending from this sector going forward. President Trump in his State of the Union address, urged Congress to pass a $1.5 trillion infrastructure package funded by public and private sector investment. Fingers crossed.

At Gerdau we monitor the CPIP numbers every month to keep you, our customers informed on the health of the U.S. construction market.