Construction Put-in-Place

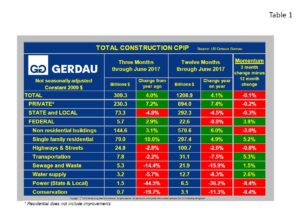

U.S. Census Bureau non-seasonally adjusted (NSA), constant dollar CPIP data showed that June total construction expenditures grew by 4.1% year on year (y/y), to $1208.9 billion (B). Private expenditures advanced 7.4% y/y, while, State & Local contracted by 4.5% y/y. Non-residential CPIP increased by 6.0% y/y to $570.6B led by strong performances for Commercial, Office, Multi-story-residential, Lodging and Recreation.

Total Construction: Table 1  presents CPIP data for total construction for both three and 12 month y/y metrics. Momentum defined as 3 month minus 12 month is also shown. Momentum provides market direction with green indicating stronger activity and red indicating slowing activity. Private construction accounted for 74.4% of the total three months expenditures ending in June. State & local spending accounted for 23.6%, leaving 2.2% for federally financed projects. The private sector posted 4.1% and 4.0% growth for 3 and 12 month y/y comparisons resulting in flat momentum.

presents CPIP data for total construction for both three and 12 month y/y metrics. Momentum defined as 3 month minus 12 month is also shown. Momentum provides market direction with green indicating stronger activity and red indicating slowing activity. Private construction accounted for 74.4% of the total three months expenditures ending in June. State & local spending accounted for 23.6%, leaving 2.2% for federally financed projects. The private sector posted 4.1% and 4.0% growth for 3 and 12 month y/y comparisons resulting in flat momentum.

The rate of growth has been slowly falling in percentage terms, yet has remained positive for 69 consecutive months. Single family residential construction recorded 10.0% growth on a three month basis, far stronger than the 4.9 %, 12 month y/y score. A momentum score of 5.2% indicated strong future growth. National building permit volume has exceeded starts volume for the past few months supporting this data.

State and local total construction contracted further this month, off 4.5% on a rolling 12 month and negative 4.8%, on a three months y/y basis. This value been negative for ten months in a row. Momentum was slightly negative at -0.3%.

Federal construction spending on the 3 month total rose 2.9% y/y to $5.8B, up from negative 0.9% on a 12 month basis, leading to 3.8% positive momentum. This makes two months in a row of positive growth recorded for the rolling three month after a string of 12 months of declining y/y results.

The infrastructure project groups posted negative growth for both 3 and 12 month y/y comparisons across the board ranging from -44.5% / -36.2% for 3 and 12 months y/y, for Power at the State and Local level to -2.2% / -7.5%, 3 and 12 months y/y, for Transportation. The only bright spot here is the positive momentum recorded for Transportation (+5.3%), Sewage & Waste (+1.5%) and Water Supply (+2.6%).

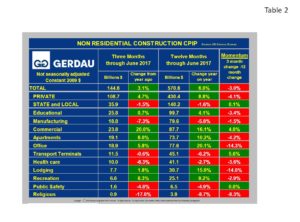

Non-residential Construction: Table 2 shows the breakdown of non-residential construction (NRC). The overall growth rate was 3.1% on a 3 month y/y basis and 6.0% on a 12 month y/y comparison resulting in -3.0% momentum.

shows the breakdown of non-residential construction (NRC). The overall growth rate was 3.1% on a 3 month y/y basis and 6.0% on a 12 month y/y comparison resulting in -3.0% momentum.

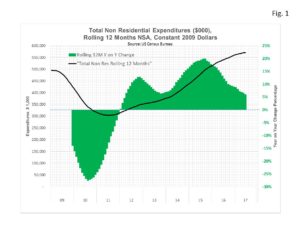

The growth rate of private NRC was 4.7% for the three months ending June, less than the rolling 12 month value of 8.8% but still showing strong growth. Figure 1 charts the NSA rolling 12 month expenditure history from 2009 to present. Expenditures (black line) are read on the left Y axis in constant 2009 dollars. The year on year change, (green bars) are read off the right Y axis. Total non-residential expenditures are at the highest level since our history began.

charts the NSA rolling 12 month expenditure history from 2009 to present. Expenditures (black line) are read on the left Y axis in constant 2009 dollars. The year on year change, (green bars) are read off the right Y axis. Total non-residential expenditures are at the highest level since our history began.

Looking at the project categories within non-residential buildings, some are strong while others are declining. Commercial, apartments (>4 stories), office, education, lodging and recreation construction are all witnessing growth on both 3 and 12 month rolling total y/y metrics. These range from 1.8% for lodging (rolling 3 month y/y), to 20.0% for commercial construction. Sectors that are recording contracting expenditures (rolling 3 month y / y), include: manufacturing buildings, transport terminals healthcare, public safety and religious structures. These range from -17.0% for Religious structures (rolling 3 month y/y), to -0.6% for Transport terminals.

At Gerdau we monitor the CPIP numbers every month to keep you, our customers informed on the health of the US construction market. The present market continues to record solid gains in the private sector, while the public sector continues to underperform.