The Baltic Dry Index

The September BDI three month moving average jumped 17.3% month on month (m/m) and surged 54.5% on a year on year, (y/y) comparison. The BDI has averaged 1,022 over the past 12 months, ranging from a low of 759 to a high of 1,364. The highest level of 1,364 was this month’s reading

The BDI is a shipping and trade index created by the London-based Baltic Exchange that measures changes in the cost to transport raw materials. The Baltic Dry Index offers a forward view into global supply and demand trends. A rising index can indicate a strengthening global economy. A contracting BDI index signals a slow-down.

The BDI includes three component ships: Capesizes, Panamaxes and Supramaxes. Capesize ships are the largest at >100,000 dead weight tons, (DWT). Capesize vessels make up 10% of the world fleet but account for 62% of dry bulk traffic. Panamaxes account for the vast majority of steel and its raw material freight, they weight in the range of between 60,000 to 80,000 DWT. Panamaxes account for 19% the world fleet and 20% of dry bulk traffic. Supramaxes (35,000 to 59,000 DWT), make-up 37% of the world fleet and combined with the smallest Handyman vessels (15,000 to 35,000 DWT), which account for 34% of the world fleet tally the remaining 18% of dry bulk traffic. Handymaxs are not counted in the BDI index.

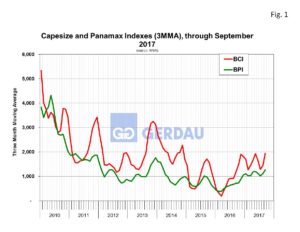

Figure 1 shows the 3MMA for both Capsize and Panamax indexes. These volatile indexes have both been trending higher since early 2016. Despite the recent rise, the BDI is still quite low compared to the 4,000 to 5,000 levels experienced in 2010. The September Capsize (BCI), 3MMA was up 34.4% m/m and up 64.0% y/y. The last three month’s actual readings were 999, 2,094 and 2,727, showing a solid upward trend. The September Panamax (BPI), 3MMA was up 13.6% m/m and up 76.0% y/y. The last three month’s actual readings were 1,146, 1,235 and 1,411, also showing a pronounced upward trend.

Figure 1 shows the 3MMA for both Capsize and Panamax indexes. These volatile indexes have both been trending higher since early 2016. Despite the recent rise, the BDI is still quite low compared to the 4,000 to 5,000 levels experienced in 2010. The September Capsize (BCI), 3MMA was up 34.4% m/m and up 64.0% y/y. The last three month’s actual readings were 999, 2,094 and 2,727, showing a solid upward trend. The September Panamax (BPI), 3MMA was up 13.6% m/m and up 76.0% y/y. The last three month’s actual readings were 1,146, 1,235 and 1,411, also showing a pronounced upward trend.

The BDIs recent strength is primarily due to strong demand for capsize vessels, as the BCI soared to a 3-year high. Capesizes, which primarily transport iron ore and coal, has surged in China as it is starting to restock these commodities ahead of winter. Restocking is normal at this time of year, however, it has been more aggressive, and started earlier than usual due to the country’s planned crackdown on emissions, which will limit industrial output. Iron ore prices have been higher in recent sessions as data shows that even though China has been hastily importing iron ore, port stocks are comparatively low. This indicates that imports are being met with a genuine demand increase that will most likely result in higher import levels. Panamax demand is also heating up, and is expected to increase further in the coming weeks as harvest season gets underway.

At Gerdau we regularly monitor the Baltic Dry index since it is a leading indicator of demand for goods on a global scale. An increasing BDI signals stronger global trade which can be good for domestic business if the transactions are fairly traded.