Architectural Billings Index

The national ABI score for August moved higher by 1.8 points to 53.7 month on month, (m/m). The ABI has now been greater than 50 for seven months in a row and for 10 of the last 12 months. The August ABI was greater than 50 in all regions of the country where it has been for four consecutive months. Regional scores were: The South 55.7, Midwest 52.5, Northeast 54.3 and the West 51.3.

The Architecture Billings Index (ABI), is a leading economic indicator that provides an approximately nine to twelve month glimpse into the future of nonresidential construction spending activity. The results are seasonally adjusted to allow for comparison to prior months. Scores above 50 indicate an aggregate increase in billings, and scores below 50 indicating a decline.

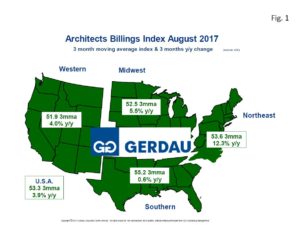

Figure 1 presents a map of the US depicting the four ABI regions. It is color coded to show expanding billings and increased growth in green and declining billings and negative growth in red. The data is shown on this map is as three month moving averages (3MMA), and 3 month year on year (y/y), percent change.

Figure 1 presents a map of the US depicting the four ABI regions. It is color coded to show expanding billings and increased growth in green and declining billings and negative growth in red. The data is shown on this map is as three month moving averages (3MMA), and 3 month year on year (y/y), percent change.

On a 3MMA basis, the U.S. ABI score was 53.3 with a 3.9% annual growth rate. The Southern zone scored the highest 3MMA ABI with 55.2. Its growth rate was up 0.6% y/y. The Northeast recorded a 53.6, 3MMA ABI and the strongest y/y growth rate at 12.3%. The Midwest posted a 52.5, 3MMA ABI, and a 5.5% y/y growth. The Western region recorded a 3MMA of 51.9 and a 4.0% y/y growth rate.

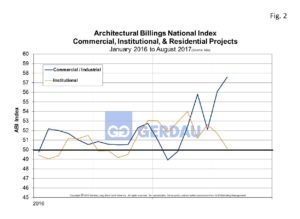

Figure 2 charts the ABI sub-index for Commercial / Industrial and Institutional from 2016 to present. The Commercial/Industrial sub-index advanced 1.5 points to 57.6 in August as the private construction sector continues to perform well. The index has been greater than 50 for 19 consecutive months. The Institutional sector scored a 50.1, down 1.6 percentage points, its tenth month in a row greater than the 50 threshold.

charts the ABI sub-index for Commercial / Industrial and Institutional from 2016 to present. The Commercial/Industrial sub-index advanced 1.5 points to 57.6 in August as the private construction sector continues to perform well. The index has been greater than 50 for 19 consecutive months. The Institutional sector scored a 50.1, down 1.6 percentage points, its tenth month in a row greater than the 50 threshold.

Table 1 lists the overall ABI and all of its sub-indexes. It presents and compares monthly and 3MMA data, showing percentage point change on both three and 12 month basis, as well as momentum. Green denotes positive change, while red indicates negative growth. National momentum, (3 month y/y subtract 12 month y/y) was positive 2.9%. Inquiries momentum was +0.2%, while Design contract momentum was up a solid 5.5%. Regionally, all four zones posted positive momentum ranging from 0.7% in the South to 7.6% in the Northeast. Multi-family residential Commercial / Industrial all recorded positive momentum. Only the Institutional project sub-index showed negative momentum, off 0.1%.

Table 1 lists the overall ABI and all of its sub-indexes. It presents and compares monthly and 3MMA data, showing percentage point change on both three and 12 month basis, as well as momentum. Green denotes positive change, while red indicates negative growth. National momentum, (3 month y/y subtract 12 month y/y) was positive 2.9%. Inquiries momentum was +0.2%, while Design contract momentum was up a solid 5.5%. Regionally, all four zones posted positive momentum ranging from 0.7% in the South to 7.6% in the Northeast. Multi-family residential Commercial / Industrial all recorded positive momentum. Only the Institutional project sub-index showed negative momentum, off 0.1%.

The construction sector employed a total of 6.918 million workers, up 28,000, (0.41%), m/m and up by 273,000, (4.11%), y/y. Most construction workers are employed constructing buildings. In August there were 1.530 million workers constructing buildings, up 5,000, (0.35%) m/m and an increase of 69,000, (4.74%) y/y. Heavy civil engineering was the next largest construction segment employing 980,500 in August, up 7,000, (0.68%) m/m and higher by 53,000, (5.74%) y/y.

Overall the August ABI report indicates continued strong growth in the non-residential construction sector.