Architectural Billings Index

At Gerdau we follow the ABI because it is a leading economic indicator that offers a glimpse into the future of non-residential construction spending of approximately 12 months. The national ABI jumped 5.3 points in December to 55.9. In an encouraging trend for future construction activity, the ABI has been north of 50 for three consecutive months. The ABI typically leads construction put-in-place (CPPI) numbers by 9 to 12 months. Regionally the Midwest recorded the strongest score at 54.4, followed by the Northeast at 54.0, the South at 53.8. The West was the only region to record a decline in demand for design services with a score of 48.8.

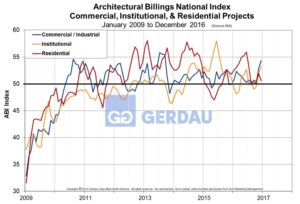

[caption id="attachment_1055" align="alignright" width="500"] Figure 1[/caption]

Figure 1[/caption]

Figure 1 charts the ABI sub-index for commercial / industrial, institutional and multi-story residential (MSR) projects from 2009 to present. Commercial/Industrial and Institutional sub-indexes surged to 54.3 and 53.3 respectively, while the MSR scored a 50.6.

Figure 2 presents awards for design contracts and measures the trends in new design contracts at architectural firms which provides a strong signal of future billings. The design contract index moved into positive territory in December with a 51.2, now north of 50 (expansionary) for two months in a row after falling to 48.7 in December.